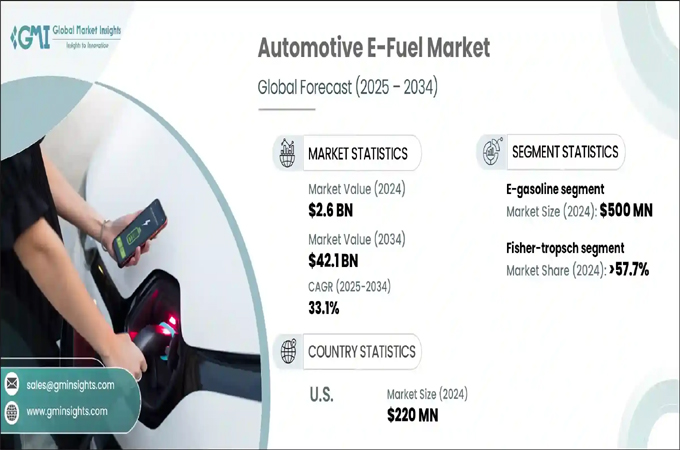

The global automotive e-fuel market is expected to reach a value of $42.1 billion by 2034, growing at a compound annual growth rate (CAGR) of 33.1 per cent from 2025 to 2034.

Governments are using strict emissions regulations to encourage the use of e-fuels to reduce greenhouse gas emissions, offering financial incentives for companies to develop sustainable fuel technologies, according to a report by Global Market Insights.

E-fuels are considered a sustainable option for reducing emissions in sectors where electricity supply is not feasible, including aviation and shipping.

Expanding e-fuels production will help meet the growing demand for sustainable alternatives to traditional fossil fuels.

E-fuels are compatible with existing gasoline and diesel engines, making them a cost-effective solution for reducing carbon emissions without requiring immediate replacement of vehicle fleets.

This makes them a versatile option for reducing emissions in transportation sectors that are difficult to convert to electricity.

In 2024, the US DOE 45ZCF-GREET guidelines listed renewable gasoline (HEFA-derived e-gasoline) as meeting ASTM D4814, signifying that drop-in e-gasoline can be used directly in existing gasoline engines and supply chains without alteration.

E-fuels reduce reliance on oil imports by offering a domestic alternative and enhance fuel supply stability by providing a storable liquid energy source, ensuring consistent availability.

Using renewable energy to make e-fuels ensures they are carbon-neutral, cutting overall emissions compared to fossil fuels.

In 2024, US EIA data show motor gasoline imports fell by 75,000 b/d to 651,000 b/d, and DOE projects that scaled e-fuel production could further decrease oil import dependence.

Manufacturers aim to reduce carbon emissions and implement eco-friendly production processes to minimise their environmental impact and enhance their reputation among consumers.

This commitment is leading to more investment in technologies that reduce carbon emissions, including hydrogen fuel cells and biofuels.

For instance, Brazil’s Ministry of Mines and Energy approved GM’s $1.42 billion investment to produce ethanol-capable hybrid-flex vehicles, leveraging local biofuels policies to lower transport emissions.

Energy firms and automakers are collaborating to build e-fuel production and distribution networks, leveraging their expertise to create efficient and sustainable energy solutions for the transportation sector.

These partnerships aim to accelerate the transition to cleaner energy sources and reduce carbon emissions in the transportation sector.

The rising consumer ESG pressure and demands for sustainable options push manufacturers to offer e-fuel-compatible vehicles to meet evolving consumer preferences.

This shift towards environmentally friendly products is motivated by an increasing awareness of how conventional gasoline-powered vehicles impact the environment.

Efforts are concentrated on reducing costs along the e-fuel supply chain, with a specific emphasis on expanding green hydrogen production.

For instance, in 2024, global electrolyser CapEx fell by about 45 per cent compared to 2021, enabling green hydrogen scale-up and cutting e-fuel production costs throughout logistics and processing.

The global market for automotive e-fuel was valued at $1.9 billion, $2 billion, and $2.6 billion in 2022, 2023, and 2024, respectively.

The market is segmented into e-gasoline, e-diesel, e-kerosene, ethanol, and e-methanol.

The US automotive e-fuel market is valued at $160 million, $170 million, and $220 million in 2022, 2023, and 2024, respectively.

This market is driven by strong R&D investment, tech innovation, and state-level policies.

The European automotive e-fuel market is expected to grow at a CAGR of 31.6 per cent till 2034, driven by strict emission regulations and ambitious carbon-neutral targets.

Major policy frameworks and government funding accelerate e-fuel production and adoption across all transport sectors.

The Asia Pacific automotive e-fuel market is estimated to reach $6.2 billion by 2034, with the region prioritising technological development and e-fuel integration to meet growing energy demands.

The push for sustainable energy solutions is fuelled by increasing awareness of climate change and the need for cleaner alternatives.

Japan reaffirmed its Basic Hydrogen Strategy in 2023, aiming for 15 GW of water electrolyser installations by 2030.

The Middle East & Africa automotive e-fuel market is expected to grow at a CAGR of 33.3 per cent up to 2034, with growing investments highlighting the region as a future low-cost e-fuel producer and exporter.

The Latin America automotive e-fuel market is expected to grow at a CAGR of 32.2 per cent till 2034, with abundant renewable resources for cost-competitive green hydrogen production.

The top four companies in this market are Porsche, HIF Global, Arcadia eFuels, and Norsk e-Fuel, accounting for approximately 30 per cent of the market share.

These firms focus on producing synthetic fuels using renewable energy, green hydrogen, and captured CO2, enabling near carbon-neutral operation of ICE vehicles and supporting decarbonisation in the automotive sector.

Porsche has heavily invested in e-fuel production to complement its electromobility strategy, particularly for high-performance ICE vehicles. -OGN / TradeArabia News Service