Carbon capture, utilisation, and storage (CCUS) is rapidly emerging as a key solution in the global energy transition, offering a realistic path to decarbonise hard-to-abate sectors such as cement, steel, refining, and thermal power generation.

Oil and gas companies are playing a leading role in the development and deployment of CCUS.

As of 2024, more than 70 per cent of the operational and planned CCUS facilities are associated with energy assets.

This indicates a growing commitment by the energy sector to reduce its emissions intensity through innovation in carbon capture and storage technologies, says GlobalData, a leading data and analytics company.

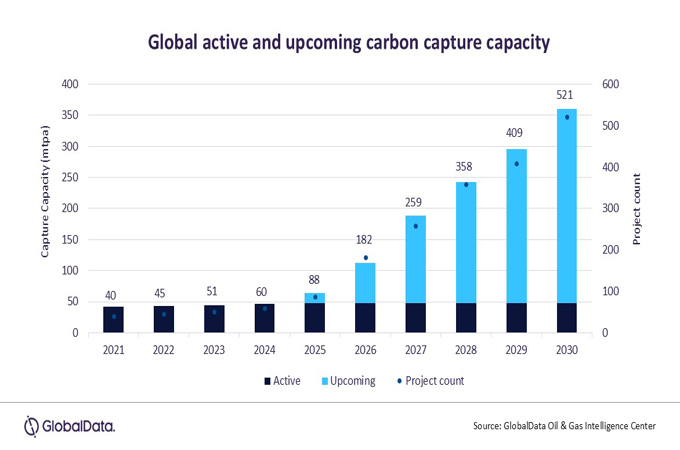

GlobalData’s Strategic Intelligence report, “Carbon Capture and Storage,” reveals that over 50 commercial-scale carbon capture projects were active within the global energy sector alone as of 2024, representing a cumulative carbon capture capacity of approximately 45 million tonnes per annum (mtpa).

Assuming that all the proposed projects come online, the global carbon capture capacity in the energy sector could rise to nearly 316 mtpa by 2030.

Leading oil and gas players such as ExxonMobil, Occidental Petroleum, and Equinor have taken early initiatives in CCUS, supported by engineering and service companies like Technip Energies, Mitsubishi Heavy Industries (MHI), and SLB.

These firms are leveraging their deep expertise in industrial-scale project delivery to develop and execute carbon capture strategies across upstream and downstream operations.

According to GlobalData’s report, there are 17 carbon capture projects in advanced stages of development that are expected to begin operations later this year. Additionally, around 460 capture projects are under development globally across diverse industries, which will lead to significant capacity growth through 2030.

Ravindra Puranik, Oil and Gas Analyst at GlobalData, comments: “Unlike consumer-driven clean energy trends, CCUS adoption is largely influenced by regulatory and economic frameworks, with limited visibility to end users. Policies such as the EU Emissions Trading System (ETS), Canada’s carbon pricing mechanism, and the US 45Q tax credit have been instrumental in unlocking commercial opportunities for CCUS. These frameworks have helped offset the high capital and operational costs of CCUS deployment, particularly in energy-intensive industries, and are driving the emergence of large-scale projects globally.”

Puranik concludes: “Despite its momentum, CCUS still faces a range of challenges that threaten to slow its scale-up. Key among these are the high upfront costs, the lack of fully developed CO₂ transport and storage infrastructure, and limited commercial applications for captured CO₂. Retrofitting existing facilities often adds further complexity, making project economics difficult without consistent policy support.

“Additionally, regulatory uncertainty around permitting processes, cross-border CO₂ transport, and long-term liability for stored carbon continues to pose risks for investors. Public skepticism also persists, with some critics viewing CCUS as a strategy to extend the life of fossil fuels rather than as a legitimate tool for emissions reduction. The absence of standardisation and the fragmented nature of the CCUS value chain further limit the ability to implement integrated, scalable solutions.” -OGN / TradeArabia News Service